Edu 2: Global Hidden Debt; FX Swaps

In this issue, I will delve deeper into the dollar funding markets, in particular the FX swaps market.

Global Hidden Debt: FX Swaps

In this issue of education piece, I will continue delving into the dollar system with an emphasis on the FX swaps market. This market has always been referred to as the “hidden debt” by numerous media outlets. If one is unfamiliar with the accounting conventions behind FX swaps, one may be led astray by the typical fear-mongering media and simply believe it’s the usual “bad practices” by banks and NBFIs. That said, it’s not.

Fig 1: $65 Trillion of Derivatives Debt Sparks Concern (Bloomberg)

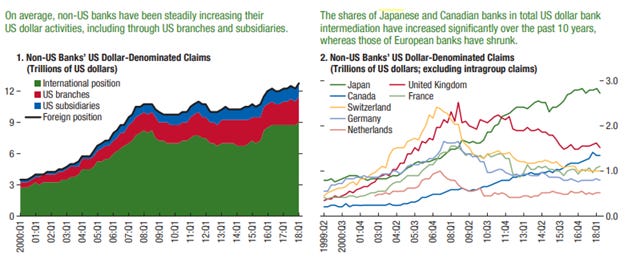

Relating to the previous piece, we know that the dollar acts as “oil” for the global financial engines. The on-balance sheet dollar-denominated assets of offshore banks have increased steadily over the past decades. Although there is a shift in geographic composition (I.e. EU banks have decreased activity after the Eurozone Debt Crisis, whilst Japan and Canadian banks have stepped up).

Fig 2: Trends in US dollar activities of Non-US Banks (International Monetary Fund)

Unlike US banks, offshore banks do not have access to stable dollar deposits, nor can they easily tap into their US subsidiaries. As a result, the dollar intermediation of offshore banks is largely dependent on “wholesale” funding (I.e., FX Swaps, Repos, CPs, interbank deposits). 50% of such Eurodollar activity is funded in these short-term wholesale markets.

In practice, when an agent wants to acquire US dollars on a hedged basis, there are 4 routes to go about it.

1) Borrow dollars on an uncollateralized basis

2) Buy spot dollars and enter into a forward contract.

3) Repo collateral for dollars

4) FX Swaps/Forwards

However, unsecured interbank borrowing markets have shrunk considerably post-GFC as banks have reduced bilateral exposure to one another (I.e. reduced counterparty risk). Hence, route 1 may not be feasible.

For route 2, an FX forward contract requires the seller of the contract to deliver the agreed amount at a pre-determined FX rate at a future date. This means that the seller of the contract typically has revenue streams of dollars that are atypical of offshore banks (if not why would they involve themselves in the wholesale market)

This leaves routes 3 & 4, and for this issue, I will mainly talk about the FX markets (i.e. Route 4)

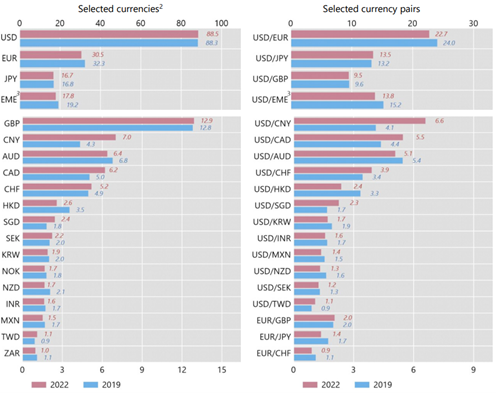

Here are some statistics from the Triennial Central Bank Survey. And as always, the US dollar remains the world’s dominant vehicle currency – 88% of all trades are traded with the dollar on one side, with Euro, Yen, and Sterling (the next 3 largest) only a fraction of dollar turnover.

Fig 3: FX market turnover by currency and currency pairs (Bank of International Settlements)

Note that they don’t add up to 100% as a single FX trade involves 2 currencies.

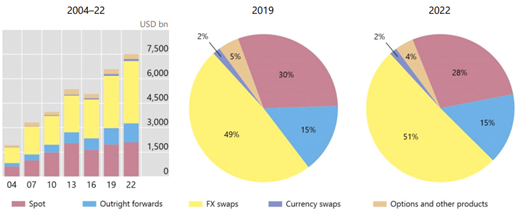

In April 2022, turnover in OTC FX markets averaged around $7.5T per day, with FX swaps and forwards accounting for the majority of the turnover in FX markets.

Fig 4: FX market turnover by instrument (Bank of International Settlements)

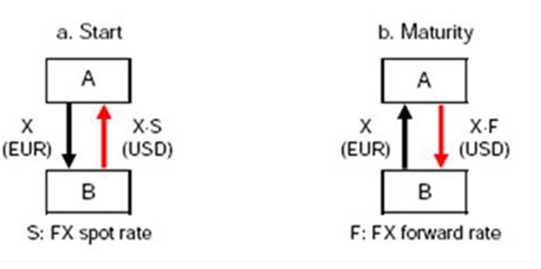

One can think of an FX swap as a contract made up of 2 separate transactions or in industry lingo ‘legs’. In the first leg, a cash sum held in one currency is exchanged for another foreign currency at the prevailing spot rate. In the second leg, a reversal exchange occurs, where the original lender receives his local currency and hands back the foreign currency at a forward rate. Effectively, currencies are “swapped”.

In essence, an FX swap is a bundle of a spot transaction and a forward transaction.

To give an example, imagine BNP Paribas (BNP), a large European bank requires dollars to pay off one of its dollar liabilities. It enters into an FX swap with Goldman Sachs (Goldman), a large US bank. Assuming that the principal of the transaction is EU$100M, the spot rate is 1.07 Dollars per Euro, and the forward rate is 1.10 Dollars per Euro

On the first leg (spot transaction), BNP hands over EU$100M and receives US$107M.

EU$100M X 1.07 = US$107M

In the second leg (forward transaction), BNP receives its EU$100 M back and pays US$110M back to Goldman at the forward rate.

EU$100M X 1.10 = US$110M

Fig 5: Description of a EUR/USD dollar swap (Oracle)

Alternatively, one can think of an FX swap as a currency loan collateralized by another currency, akin to repo where the collateral is normally a security.

Additionally, FX and currency swaps differs to traditional Over-The-Counter (OTC) derivatives. In FX and currency swaps, notional amounts exchanges hand at the start and the end of the contract as opposed to acting as a reference for smaller amounts being exchanged (i.e. Vanilla fixed-to-floating interest rate swaps as an example)

Back to the topic, non-US banks gross exposure to FX swaps and forwards exceeds $30T, more than double their gross on-balance sheet dollar debt standing at $13T. Additionally, NBFIs outside the US have about $18T outstanding in FX swaps and forwards, larger than their on-balance sheet debt at around $12T.

This is due to the accounting treatment of FX swaps differing greatly in comparison to their secured counterparts. Other forms of collateralised borrowing are recorded on-balance sheet whilst FX swaps are recorded as off-balance sheet and only appears in the footnotes. This gives rise to its ‘hidden’ characteristics and consequently, its not rare to find off-balance sheet debt worth multiple times its on-balance sheet assets.

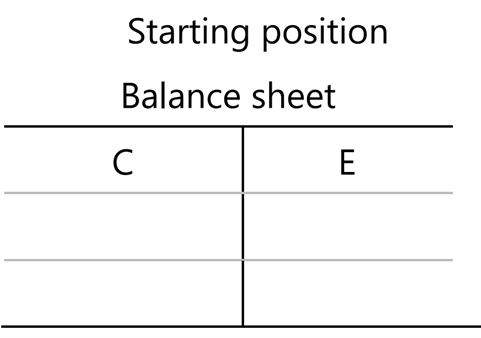

So how does an FX swap transaction actually appear on the balance sheet?

Assuming that a Japanese agent begins his holdings with Japanese Yen (C). This is appeared on the balance sheet as Currency on the Asset Side and Equity on the Equity Side.

Fig 6: Initial Balance Sheet (BIS)

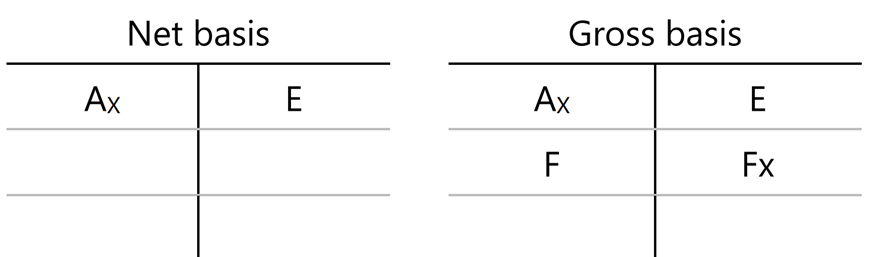

To acquire a foreign asset (i.e. USTs) on a hedge basis, the agent can enter into a spot transaction to exchange yen for dollars and simultaneously enter into a forward contract. The dollars is then used to acquire USTs (indicated as Ax on the Balance sheet).

The forward contracts creates an future obligations to pay in dollars (liability of Fx on the Balance sheet), matched by the right to receive the domestic currency (asset of F on the Balance sheet)

Fig 7: Post Balance Sheet (BIS)

There are 2 ways to record the transaction on a 1) Net Basis and 2) Gross Basis. On a gross basis, all rights and obligations are shown explicitly on the balance sheet. On the other hand, a net basis nets them out. Note that there is a currency mismatch when using the net basis as a foreign asset is funded by local currency.

It should be apparent by now that the combination of the spot and forward FX transactions is equivalent to an FX swap if the 2 transactions is bundled to a single counterparty as a single contract.

However, forwards and swaps are treated as derivatives so that only the net value is recorded as fair value and hence the obligations arising from them ‘disappear’ from the balance sheet. This is the reason behind the “Missing debt” but one should also note that there are too “Missing Claims/Assets” as the balance sheet have to balance after all.

Nonetheless, I do agree with BIS that the FX swaps pose some financial risk as they are the main tools of cross-border funding for dollar balance sheets of non-US entities. As explained in the earlier post, the usage of short-term funding vehicles to fund longer-tenor assets poses substantial risk if one is unable to roll over funding in an event of financial stress.

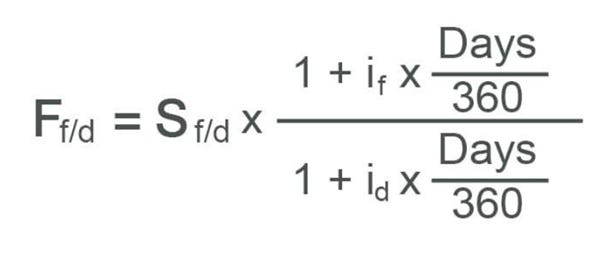

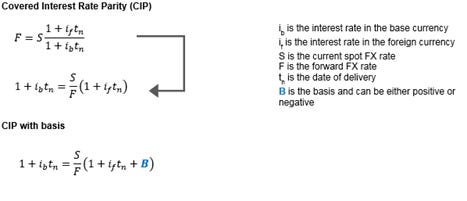

After unveiling the hidden debt story, there is something more interesting I want to talk about. It is a persistent deviation from covered interest rate parity (CIRP) in the dollar funding markets, whose theory is synonymous with physical law in international finance but has been violated for many years.

CIRP is a theoretical condition that defines the relationship between interest rates, spot, and forward currency. It states that the difference in the spot and forward rate of a currency is equivalent to the interest rate differential of the two currencies.

Fig 8: Covered Interest Rate Parity Formula (Wall Street Mojo)

Sounds confusing right?

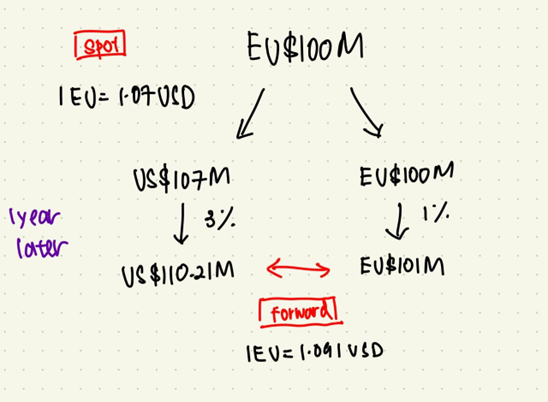

To give an example, imagine a European agent who wishes to borrow EU$100M in dollars the next year. Assuming the US interest rate is 3% and the spot exchange rate is 1.07 Dollars per Euro. The agent can exchange EU$100M for US$107M dollars at the spot rate and parks it a safe asset (i.e. USTs) yielding 3% of a year. At the end of the year, it becomes US$110.21M.

Alternatively, he can park the EU$100M in a EU bank for 1% (assuming the interest rate is 1% in EU). By the end of the year, the agent gets EU$101M and can exchange it at the forward rate (the spot rate 1 year later). And by CIRP, the forward exchange rate must fulfil that EU$101M = US$110.21M. In this case, the forward rate (or the spot rate 1 year later) would be 1.091 dollars per Euro (110.21/101)

By using the CIRP formula, we arrive at the forward rate to be 1.0911 too. In other words, a lower interest rate is compensated by a higher forward rate. It is also a no-arbitrage condition.

Fig 9: Visualisation of CIRP (Chet Wee)

Note that some macro minds out there find CIRP to be in contradiction to interest rate differentials (i.e. higher interest rates push the currency up as entities can take the opportunity for carry trades). In my humble opinion, the CIRP expects currencies to return to equilibrium over a longer time frame a couple of years), whereas an increase in short-term interest rates usually has a positive impact on the relevant currency due to higher capital flows. So, one looks at the next few years, and the other looks at the next few weeks or months.

Back to the topic, this deviation from the CIRP shows up in the cross-currency basis (XCCY basis). It is the implied dollar interest rate (cost of dollar funding) from the FX market, represented by the B in the diagram below.

Fig 10: CIP with basis (Russell Investments)

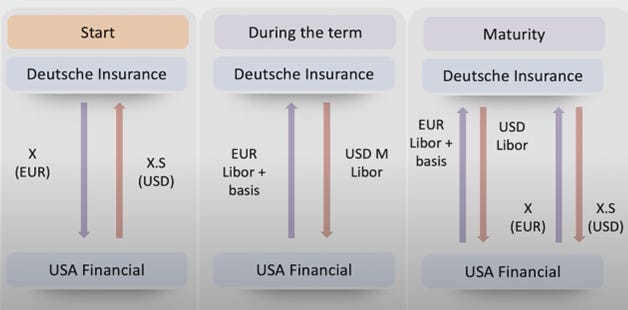

Using the EUR/USD example above, a negative basis means that the European agent needs to pay 3% in dollars while only receiving 1% + (-b) in Euro in interest payments in a cross-currency swap.

Fig 11: Basic Mechanics of a Cross-Currency Swap (Analyst Prep)

Note that, a currency swap serves an almost equivalent function to an FX swap, but it involves interest rate payment flows for the duration of the contract. Normally, FX swaps are short-term duration contracts whilst currency swaps are longer duration contractions. In this light, an FX swap can be thought of as a money market instrument whereas a currency swap can be thought of as a capital market instrument.

In a nutshell, a negative basis means that borrowing through a cross-currency swap is more expensive than borrowing in the spot market. The more negative it is, the more dollar shortage in the world. This violates the no-arbitrage condition and hence CIRP as one could simply borrow dollars in the spot market and lend in the swaps market

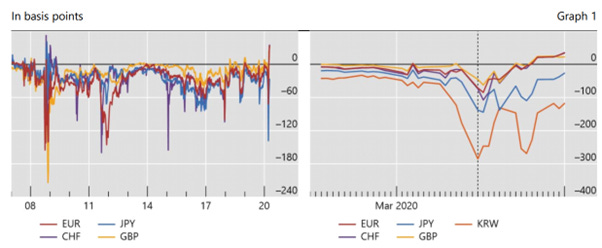

Fig 12: 3-month FX swap basis against the US dollar (Bank of International Settlements)

Some reasons for the persistent existence of a negative basis against the dollar is due to risk premiums arising from counterparty risk and a huge hedging and funding demand for dollars from offshore banks, NBFI, and non-financial firms with large dollar balance sheets.

In summary, FX swaps maintain the modal mode of cross-border dollar FX transactions and its accounting practices gives rise to it “hidden” characteristic. Due to a global demand for dollars, we see persistent negative basis and hence deviations from the CIRP.

I hope you guys enjoy this piece and I will continue to delve into the dollar mechanics in the next piece!